As more and more corporations feel external and internal pressures to improve the sustainability of their businesses as well as their bottom line, many have looked at their own energy consumption as a place for change. These companies have decided to pursue developing and acquiring renewable energy independently of their local utility.

Broadly, there are two ways to accomplish this goal. The first is for corporations to produce the energy themselves. This means installing systems like wind turbines or photovoltaic solar panels directly at their facilities and using the energy they produce on-site. This method has the added benefit of being able to show off the renewable assets. For example, the Shedd Aquarium in Chicago has built a solar system that includes battery storage located in the aquarium’s loading dock combined with solar on the rooftop.

However, directly producing power comes with a suite of other concerns, such as system maintenance, optimal placement, engineering and management of the construction project, and negotiating with the local utility over compensation for any excess power they generate. This last issue has become particularly controversial as evidenced by the debate in the solar industry over net metering.

The second option is to contract with renewable energy developers and commit to buying power from a renewable energy project. These contracts are aptly called Power Purchase Agreements (PPAs) and have lately become a popular and increasingly common method for corporations—especially large corporations—to meet their green energy goals.

PPAs, What are They and How do They Work?

PPAs are agreements between an independent electricity generator and a corporation on a fixed price for the power produced over the term of the contract. Developers do this because renewable sources like wind and solar have minimal marginal costs of running the plant, most of the costs are the high up-front capital costs of development. This allows buyers to lock in prices and hedge against power price volatility. These contracts also allow corporations to meet their sustainability goals without having to develop in-house the capability to produce it.

“PPAs play a key role in financing and developing electricity projects and have been used for years by utility companies and banks. Within the past several years, PPAs have become more widely recognized as a means for consumers to gain access to renewable energy. Large-scale PPAs are an increasingly competitive and progressive way for organizations to purchase renewable energy, hedging their fossil fuel costs and meeting their sustainability goals simultaneously.” — Renewable Choice Energy

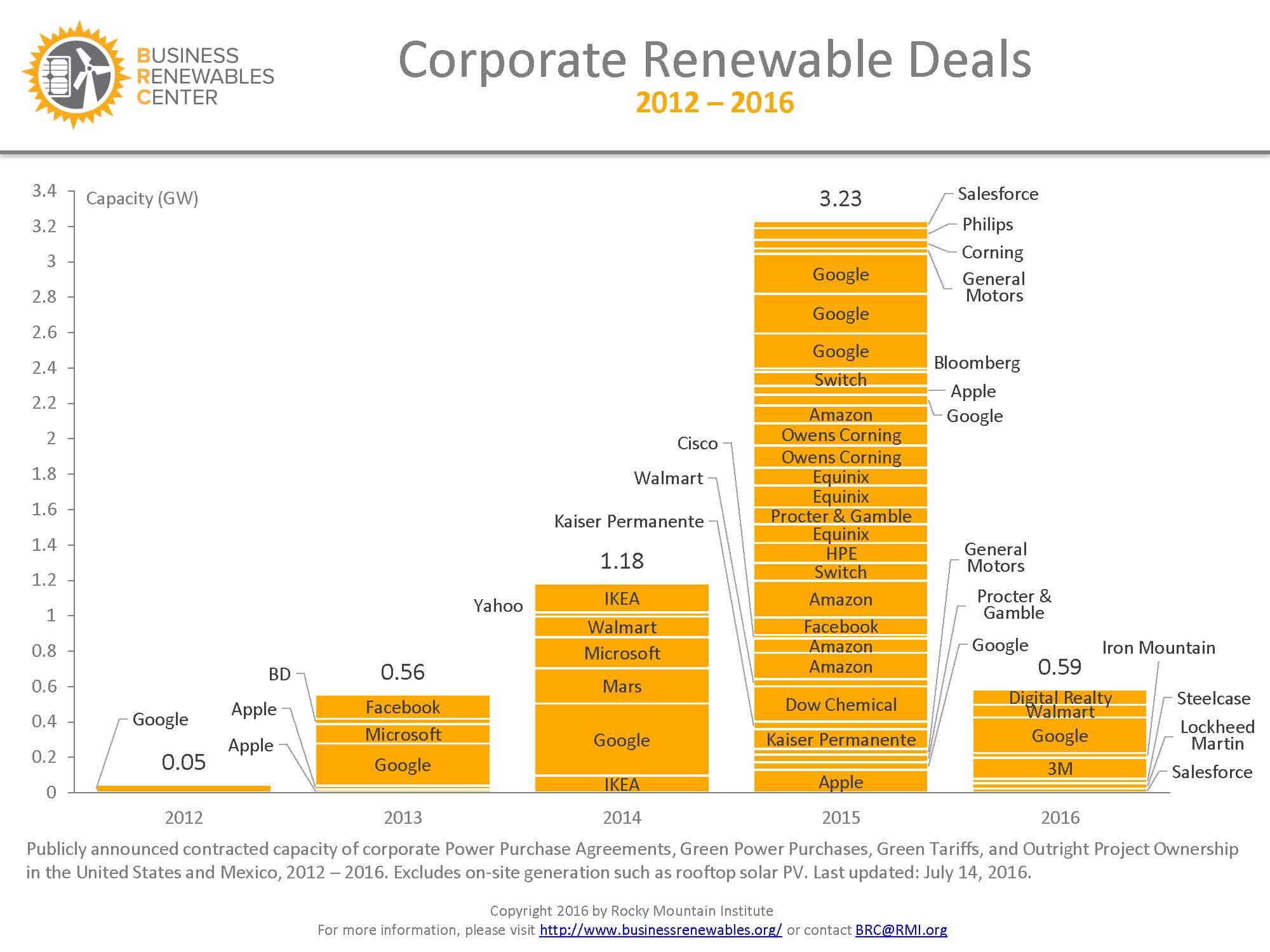

As you can see from the chart below, corporate purchases of large amounts of renewable power is growing, and this is largely due to PPAs.  Credit: Rocky Mountain Institute

Credit: Rocky Mountain Institute

All PPAs provide three main benefits:

- Fixed price on energy from the renewable sources, providing a hedge against future energy price increases and volatility

- The Renewable Energy Credits (RECs) associated with the renewable energy (more on this later)

- Steady income streams for the developer. These long-term, steady income streams are often instrumental to securing the capital required to get the project off the ground. (This is called additionality which is also covered later)

Onsite PPA

In some cases, corporations highly value having at least some renewable generation at their facilities. These might be very public places like museums, universities, or a company headquarters. To avoid worrying about running the system themselves, these corporations will work with a renewable project developer to own and manage the project on-site and then purchase the power generated. Groups who have very low to zero tax liability like churches or schools will often build in discounts to the price of the power as the producer will claim the tax breaks often associated with renewable projects.

Offsite/Direct PPA:

Since not all facilities are good locations for renewable power plants, many companies will opt for an offsite or direct PPA. In a direct PPA, the buyer again commits to pay a fixed price for the electricity that they generate but contrary to what the name might indicate, there is no direct power line between the renewable generation and the buyer’s facility. The power is generated off-site often in much larger quantities than an onsite system, allowing the company to cover far more of their operations.

To illustrate what is going on we can imagine a fictional scenario. In this case, NewCorp—our fictional corporation wanting to reduce their environmental impact—and CleanPower—our fictional renewable energy producer—have agreed to a 5 cent / kwh PPA for all the energy that CleanPower produces. As CleanPower produces energy, NewCorp purchases the energy at 5 cents/kwh and is now responsible for getting that energy to the grid including selling the power to the general markets and scheduling the delivery of the power. If the grid price, or Locational Marginal Price (LMP), for power is higher than 5 cents/kwh then NewCorp has made money.

This provides NewCorp with a hedge against rising energy prices and often the RECs associated that power. However, this means that NewCorp also has to deal with all the challenges associated with buying and selling power in an energy market.

Virtual PPA

To avoid those headaches, NewCorp might instead consider a virtual PPA. In a virtual PPA NewCorp does not directly purchase the power generated by CleanPower. Just like in a direct PPA, NewCorp and CleanPower have agreed to a set price that CleanPower will receive for the power that they produce. However, in a virtual PPA NewCorp never directly owns the energy produced.

In this new example, as CleanPower produces electricity, they sell the power onto the grid priced at the Location Marginal Price (LMP)—this price is constantly changing and determined at the regional ISO hub or project node. As this is happening, NewCorp pays CleanPower the 5 cents/kwh that they agreed to. CleanPower then turns around and gives the money from the power sale to NewCorp. In financial terms, a virtual PPA is a “fixed for floating” swap. NewCorp swaps its fixed PPA price for the floating or variable LMP of the renewable energy. If the LMP is greater than the PPA price then NewCorp makes money.

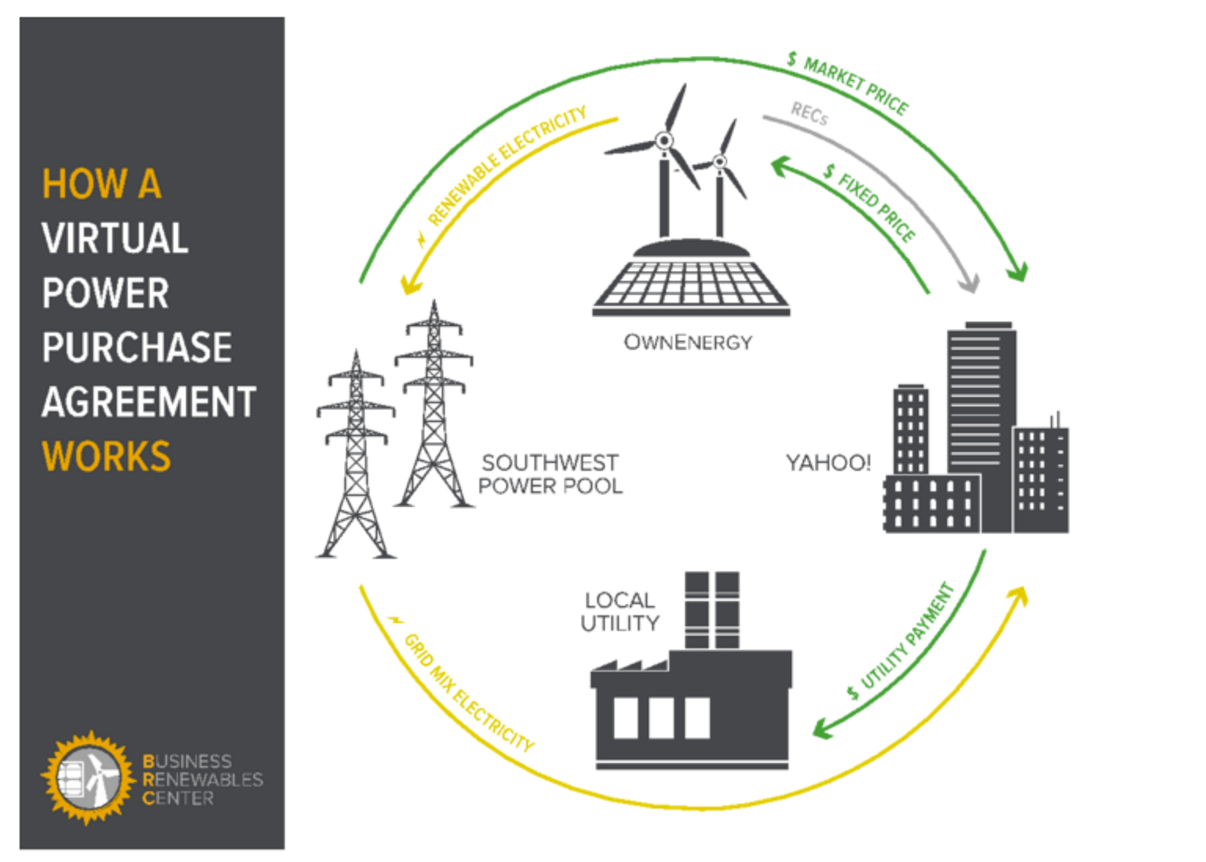

The virtual PPA achieves the same benefits of other PPAs: fixed energy costs, renewable energy benefits for NewCorp, and a stable income stream for CleanPower. But because NewCorp never owned the energy it reduces the technical challenges that NewCorp is responsible for. Below is a good graphical representation of an actual VPPA between Yahoo! and OwnEnergy from RMI’s Business Renewables Center.

PPAs and Electric Power markets

Starting in the 1970s and accelerating in 1992 with the passage of the Energy Policy Act, US electricity markets have split into two categories: Regulated markets and restructured markets. In regulated markets, utilities are vertically integrated and control all parts of the electricity system from generation to transmission to delivery. In a restructured market, utilities are only responsible for distribution, operations, and maintenance from the interconnection at the grid to the meter; billing the ratepayer; and acting as the Provider of Last Resort (POLR).[1] In these restructured markets, Independent Power Producers own and operate the power plants.

This has huge effects on where different kinds of PPAs are possible. Since in a direct PPA the corporation consumes the energy that the developer produces, most direct PPAs need to be located in restructured retail markets. In other words, independent power producers can sell their electricity directly to consumers. For a virtual PPA, the only limitation is on where the project needs to be located. These projects can be developed in any restructured wholesale market, where independent power producers are not necessarily selling their electricity directly to consumers.

To build a system that works within vertically integrated electricity markets with traditional utilities, World Resources Institute suggests building out green tariffs. A green tariff is a program administered by a utility where a customer can then source renewable energy from their local grid. This allows utilities to take on the brunt of the transactions with renewable power producers while giving corporations and other customers the benefits of green power. This would allow the utility to source a larger generation portfolio while distributing risk and optimizing for the local grid. Independent power producers could still own and operate their plants but corporations or other customers could have vastly reduced transaction costs. Utilities could even build in stable pricing to account for one of the key benefits of a PPA.

Additionality and RECs

Part of the PPA is the purchase of Renewable Energy Credits (RECs) which are a certification of the renewable attributes of the electricity. This allows the corporation to claim that they used renewable energy for their operations. However, while RECs are created by renewable projects, simply purchasing those RECs does not help drive additional renewable energy development. Instead, they account for existing projects and do not help to change the fuel mix away from fossil fuels. This additionality is a key component of PPAs.

“An additionality claim in and of itself does not convey actual environmental benefit—it is, effectively, a marketing claim. Additionality claims allow corporate buyers to make highly visible commitments that demonstrate their support for renewables because this support is essential to getting the wind or solar project off the ground.” —Renewable Energy Choice

Additionality is the ability to claim that the renewable energy project would not have existed without the corporation’s support. For many corporations, being able to credibly show their support for clean energy development overall is a primary driver in seeking ways to reduce their impact. By creating steady streams of income for renewable project developers, PPAs make sure that projects can become financially viable. These income streams are often the basis upon which developers can get access to the capital necessary to build wind or solar farms which have significant up-front capital costs. For example, Google has stressed that additionality is key for their vision. This is why they use PPAs rather than simply buying the RECs associated with the power that they need.

All of the different solutions described above meet additionality requirements. On-site systems clearly would not have been built without the corporation’s actions. This reduces their demand for grid power and replaces it with their own renewable power. Direct PPAs give renewable project developers a guaranteed purchaser of some or all of the power they generate. They also provide the long-term financial stability required to get the large capital for the project. Virtual PPAs also provide the same kind of financial stability.

Conclusion

There are many risks and challenges in PPAs that have to be accounted for. For example, there are risks of short-term losses as wholesale energy prices fluctuate. PPAs are also fairly complicated legal and financial documents. These negotiations often require corporations to bring in lawyers and other consultants to help correctly structure these deals. However, even with these challenges, PPAs still remain as the most effective and flexible way for corporations to make broad impacts to their current energy mix.

PPAs are incredibly flexible and effective tools for a variety of corporations looking to make their operations more sustainable. They provide price hedges against future price increases and volatility, the environmental benefits associated with a renewable energy project, and steady income from PPAs drives the development of new clean energy projects that help change our fuel mix. Given these benefits, we expect PPA signings to increase both in quantity and magnitude as increasing numbers of U.S. corporations look to improve their environmental impact. [1] Energy Smart